RGA Research: US population mortality

Analysis of US data provides valuable insights into emerging excess mortality

Learn more

Why U.S. post-pandemic mortality matters ... and how to track it

introduction

Stay connected

Trusted partner.

Proven results.

top of page

©2025, Reinsurance Group of America, Incorporated. All rights reserved. No part of this publication may be reproduced in any form without the prior permission of the publisher. For requests to reproduce in part or entirely, please contact: publications@rgare.com. RGA has made all reasonable efforts to ensure that the information provided in this publication is accurate at the time of inclusion and accepts no liability for any inaccuracies or omissions. None of the information or opinions contained in this publication should be construed as constituting medical advice.

Where are we? How did we get here? Where are we going?

Ready to dig deeper? Let’s talk

Coming soon: By-cause mortality reports

Read more

Hear Perspectives from the RGA experts

A wide range of RGA experts – in underwriting, pricing, risk management, insurance medicine, research and development, and more – have derived insights from this data analysis that they have applied to insured (individual and group life) and annuitant populations. Brief summaries of these insights and their ongoing value to RGA’s work can be found at the link below.

EXCESS MORTALITY ESTIMATES

March 2020 - December 2020

January 2021 - December 2021

~21%

Video: Post-Pandemic Mortality Trends Explored

All-cause mortality report

Read the report

ThE BIG PICTURE

Individual Life Actuarial “While US individual life mortality is typically thought of as being much lower than general population mortality, population mortality can still help inform assumption setting for insureds in certain areas.” Susan Willeat Vice President and Managing Actuary, Assumptions Lead in US Individual Life

Group Life Actuarial “Given reporting lags associated with group life data, US population mortality data provides early insights into emerging trends in the group life market. Further, cause-of-death data at more granular breakdowns by age and gender are more credible in the larger US population dataset.” Michelle Haines Associate Actuary in US Group Re

Financial Solutions Actuarial “US population mortality experience can help us understand mortality trends and inform assumptions for pensioners.” Emily Dave Actuary in US Longevity Research

Mortality TRENDS “US CDC population death data can serve as a high-quality leading indicator of where insured mortality improvement may be headed.” Jason McKinley Vice President and Actuary, Global Research and Development

Insurance Risk “Insured population mortality and morbidity assumptions need to be set in the context of the wider general population. The trends and changes observed within the wider population provide insights into some of the dynamics that may filter through to the insured population.” Elena Tonkovski Vice President and Senior Actuary, Insurance Risk

January 2022 - December 2022

~11%

Post-Pandemic Mortality Trends Explored

A summary look at RGA's in-depth analysis of US mortality data In this brief video, RGA's Micah Canaday, Vice President of Americas Data Solutions, explains how RGA is using CDC population mortality data to derive insights into medium-term and possibly longer-term changes.

CLOSE X

Share:

Understanding where non-COVID excess may be headed requires a comprehensive evaluation of each major cause of death and comparing current mortality with pre-pandemic expectations. To that end, subsequent reports in RGA’s analysis of US population mortality will explore the main causes of death individually to determine their contributions to the excess over time. Be sure to check back to view these by-cause reports or sign up to have RGA notify you as they are published.

Coming Soon: By-cause mortality reports

UNDERWRITING “As we emerge from the acute phase of the pandemic, our analyses of US population death data have helped us unpick the drivers of ongoing excess mortality.” Catie Muccigrosso Vice President and Chief Underwriter in US Individual Life

GLOBAL R&D ”During the COVID-19 pandemic, the CDC data offered us a near real-time opportunity to monitor both the direct and indirect death toll of the pandemic; like many researchers, we observed that the full impact of the pandemic was much greater than what was suggested by deaths due to COVID-19 alone.” Richard Russell Vice President, Biometric Research, Global Research and Development

~19%

US CDC population death data can serve as a high-quality leading indicator of where insured mortality improvement may be headed. Anyone with experience in assumption setting understands that mortality improvement is different in the insured population vs. the overall population. That’s too bad since mortality improvement is as important as assumptions get when it comes to pricing and valuation. However, with the granularity of attributes available in the population data, actuaries can develop approaches to transform the population data into something that gets closer to insured experience. CDC population data includes cause of death and, since 1989, highest education level achieved by the decedent. The education mix and the cause-of-death mix differ between insured and overall population: The education mix is a bit higher educated for insured, and the cause-of-death mix skews more towards cancer and much further from non-medical causes than the overall population. The higher education level ties to higher income, which makes life insurance more easily affordable; the cause-of-death profile ties with underwriting. After developing proper exposures for education, population data may be transformed on that axis, but perhaps more importantly, reallocating the cause-of-death profile and running out projections can reveal striking differences between the insured and overall populations. Even when modeling factors such as long-term rates and convergence periods are set equal, differences of more than 1% appear in the early projection years – with typically better improvement in the subset with higher education and a cause-of-death profile resembling an insured block. When taking these factors into account, the CDC data provides valuable insights into the potential direction of improvements in insured mortality.

Jason McKinley

Actuary in Global Research and Development

next expert

prior expert

US population cause-of-death data helps us monitor how past and present medical advances have driven down mortality rates, and project how cause-specific mortality rates will evolve in future years. The dramatic extension of life expectancy is perhaps the pinnacle of public health and medical achievements in the 20th century. Before the COVID-19 pandemic, US life expectancy had increased steadily over many decades, although this trend stalled between 2012 and 2019. Life expectancy is a key marker of social progress, reflecting medical, economic, environmental, and societal influences. Some significant drivers of past improvements in mortality include: (1) advances in medical technology such as vaccines and antibiotics; (2) public health initiatives such as clean water sourcing, sanitation, and smoking cessation programs. Take cancer as an example. Over the past 30 years, the US has celebrated a string of cancer success stories that have helped to significantly lower the nation’s cancer mortality rate. Improvements in cancer screening and treatment, such as adjuvant chemotherapies and immunotherapies, mean considerably more people now survive a cancer diagnosis. Some forms of cancer that were once incurable are now manageable, and the opportunity for cancer survivors to obtain life insurance has increased correspondingly over time. The US has a lower life expectancy than many peer countries, but promising advances will likely drive meaningful increases in life expectancy in the future. These advances include precision medicine (such as multi-cancer early detection tests and personalized cancer therapy), obesity treatments, and artificial intelligence.

Dr. Daniel Zimmerman

SVP and Chief Science Advisor

During the COVID-19 pandemic, the CDC data offered us a near real-time opportunity to monitor both the direct and indirect death toll of the pandemic; like many researchers, we observed that the full impact of the pandemic was much greater than what was suggested by deaths due to COVID-19 alone. Our research – using CDC data – has also helped us to estimate the proportion of excess mortality that was a direct result of a SARS-CoV-2 infection. To apportion excess deaths into those directly attributable to SARS-CoV-2 infection and those indirectly associated with the "ripple effects” of the pandemic, multiple drivers of cause-specific mortality – and changes in these during the pandemic period – need to be carefully examined. One example of a significant change in cause-specific mortality, in the pandemic period, is the decrease in influenza deaths seen in the first three months of 2021. Another example is the count of deaths due to cardiovascular disease (CVD) – this grew significantly in 2020, from 874,613 CVD-related deaths recorded in 2019 to 928,741 in 2020.

Richard Russell

VP in Global Research and Development

Insured population mortality and morbidity assumptions need to be set in the context of the wider general population. The trends and changes observed within the wider population provide insights into some of the dynamics that may filter through to the insured population. This can be helpful in identifying emerging areas where actual experience may deviate from expected experience. For example, the stalling of cardiovascular mortality improvements observed for the working-age population in recent years has filtered through to the insured population experience. Looking to the future, promising medical advancements that, depending on their efficacy and availability to the wider population, may first manifest observable benefits in population data ahead of less credible insured life data.

Elena Tonkovski

VP and Senior Actuary, Insurance Risk

Insurance Risk

global r&d

insurance medicine

mortality trends

As we emerge from the acute phase of the pandemic, our analyses of US population death data have helped us determine the drivers of ongoing excess mortality. For instance, many individuals with SARS-CoV-2 infection experience symptoms that persist far beyond the immediate phase of the disease, sometimes lasting for years after the initial acute illness. Research shows that among individuals hospitalized for COVID-19, risk of death declined but remained significantly elevated in the third year after infection. Further, the three-year burden of cardiovascular disease in hospitalized survivors of acute COVID-19 is also substantial. This likely helps to explain why increases in cardiovascular mortality rates – observed at the height of the COVID-19 pandemic – endured well into 2023, despite the end of the public health emergency.

underwriting

Catie Muccigrosso

VP and Chief Underwriter in US Individual Life

US population mortality experience can help us understand mortality trends and inform assumptions for pensioners. While, in general, pensioner mortality differs from the general population, population mortality can be useful in providing insights due to its comprehensive nature and diverse demographic coverage. The population data is valuable in identifying trends in life expectancy, comparing regional differences, and determining and projecting cohort effects, which requires large datasets. It is particularly useful in areas where pensioner data is sparse, such as for ages above 90 years old. By analyzing population data at a cause-of-death level, we can gain insights into the key influences on, and reasons for, overall mortality outcomes for specific age groups, which helps us to understand past trends. This analysis, coupled with additional research, aids in predicting how mortality may evolve in the future and provides a basis for scenario testing.

Financial Solutions Actuarial

Emily Dave

Actuary in US Longevity Research

Given reporting lags associated with group life data, US population mortality data provides early insights into emerging trends in the group life market. Further, cause-of-death data at more granular breakdowns by age and gender are more credible in the larger US population dataset. That said, we know group life mortality is lower than the general population, with the "SOA 2016 Group Term Life Mortality Study" showing insured mortality at 30%-40% of population mortality in the key working ages. The actively-at-work requirement for employees covered by group life leads to a healthier subset and is the main driver for this differential. During the COVID-19 pandemic, insured mortality remained lower than population mortality, and excess mortality was directionally in line with the US population. By studying the relationship between recent insured and population excess mortality, actuaries can estimate population-to-insured factors to apply to projected population excess mortality. This in turn helps set assumptions for future expected excess group life mortality.

Group Life Actuarial

Michelle Haines

Associate Actuary in US Group Re

While US individual life mortality is typically thought of as being much lower than general population mortality, population mortality can still help inform assumption-setting for insureds in certain areas. One area is final expense, which generally serves a lower socioeconomic group very different from typical fully underwritten business. No current industry mortality table is even close to appropriate for final expense business. We have found that US population tables provide the best baseline table for developing our internal mortality assumptions for final expense. Final expense mortality increases relative to population as age decreases. The US population baseline also provides useful perspective on the mortality for this unique market segment. US population mortality is also helpful in setting mortality assumptions for very high attained ages. US individual life mortality experience is clearly not as credible at very high attained ages as population experience. The question often arises: Will insured and population mortality eventually converge at some attained age? In other words, will the socioeconomic impacts that drive the difference between insured and population mortality disappear? One can use population mortality data split by a proxy for socioeconomic class to provide an indication of any convergence that could potentially inform assumption-setting at very high attained ages. By comparing the high attained age assumptions for each of our various market segments to a US population basis, we can easily review them for consistency.

Individual Life Actuarial

Susan Willeat

VP and Managing Actuary, Assumptions Lead in US Individual Life

In the wake of the COVID-19 pandemic, recent years’ data is not a reliable predictor of future mortality, and actuaries can no longer steer assumptions by just looking back. Using the CDC’s weekly updated WONDER data base, RGA has conducted a thorough analysis of emerging data to identify how US mortality has changed through the pandemic, determine what it looks like in the short term, and understand where it may be headed in the coming years. RGA’s analysis shows that while excess mortality has persisted in the US population following the acute phase of the pandemic, recent mortality trends – including 2024 excess death estimates – suggest that the overall excess has decreased substantially from the acute-phase peak. This digital report provides an overview of that analysis, an investigation of all-cause mortality, and perspectives on the report’s implications from experts across RGA's functions. In the coming months, the report will break down US mortality by principal causes.

make sure links are live

Insurance Medicine “US population cause-of-death data helps us to monitor how past and present medical advances have driven down mortality rates, and project how cause-specific mortality rates will evolve in future years.” Dr. Daniel Zimmerman Executive Medical Editor and Advisor Executive Strategy

January 2023 - December 2023

~3%

January 2024 - December 2024

~0.4%

Key takeaways In the current post-pandemic era, the observed short-term changes in population excess mortality are offering insight into medium-term and possibly longer-term changes. RGA has conducted an analysis of emerging US population mortality experience using three essential components: up-to-date death data from the CDC, population estimates from the US Census Bureau, and RGA developed pre-pandemic expectations of mortality against which the observed mortality can be compared and the excess calculated. US population mortality is a key source of granular and current mortality experience. Emerging US results may provide leading insights into mortality trends in insured lives applicable to multiple markets and multiple functions within an insurer.

Key takeaways

Ebrahim Steenkamp Data Scientist, Global Research and Development

Dan Brandt Vice President and Actuary, Experience Studies & Analytics, U.S. Individual Life

Michelle Haines Associate Actuary, Life, Accident and Worksite, U.S. Group Reinsurance

Jason McKinley Vice President and Actuary, Global Research and Development

Brendon Lapham Director, Data and Analytics Actuary, UK Pricing

Micah Canaday Vice President, Data Commercialization Global Data and Analytics

Richard Russell Vice President, Biometric Research, Global Research and Development

How to monitor US population mortality Monitoring emerging mortality experience requires three essential components: up-to-date death data, exposed-to-risk (exposure) data, and some expectation of mortality against which observed mortality can be measured. The US Centers for Disease Control and Prevention (CDC) National Center for Health Statistics (NCHS) provides authoritative US death data. Finalized death data through year-end 2022 is currently available from the CDC NCHS Vital Statistics Online Data Portal.2 Provisional and incomplete death counts are available from CDC NCHS’s mortality data via CDC’s Wide-Ranging ONLine Data for Epidemiologic Research (WONDER),3 the CDC portal for public health data, through the end of the prior week. Data are based on death certificates for US residents; each death certificate contains a single underlying cause of death, up to 20 multiple causes of death, and a myriad of demographic data. Death counts from CDC WONDER can be obtained pre-stratified by several variables, including place of residence (total US, region, state, and county), age group (including single-year-of-age cohorts), gender, date of death, place of death, and cause of death. Users must exercise care and judgment when using the latest mortality data from WONDER. (See “Considerations for death data” in this paper for more on this.) Raw death counts provide minimal value without exposure data. Exposure data must correspond to death data or be adjusted accordingly. The US Census Bureau (USCB),4 the official arbiter of national population numbers, provides both population estimates and projections, which can be used to develop exposure estimates. Alternative population estimates are available from other sources, but those estimates require careful review to ensure they correspond to the death data and cover all age ranges.

Understanding how current mortality has changed compared to pre-pandemic expectations requires an expected mortality basis, i.e., some form of expected mortality, against which to measure. Expected mortality is critical to determining excess mortality and its likely trajectory. (Considerations for expected mortality are explored later in this article.) Understanding changes in the drivers of mortality requires identifying underlying causes of death and breaking down expected mortality by cause. The cause definitions in the expected basis must align with the cause definitions in the death data to ensure they are comparable. This may sound obvious and straightforward, but anyone who has tried to reconcile causes of death across multiple International Classification of Disease (ICD) versions knows it is neither.

It is important to note that the USCB revises population estimates periodically as new data becomes available and methods are refined. Because of this, both population and exposure estimates can change, and results may change accordingly. By fall of 2024, the USCB expects to release the 2010 to 2020 Intercensal Estimates – the official population estimates for the 2010-2020 decade.

Considerations for death data Just as there are incurred but not reported/recorded (IBNR) claims in the insurance world, there are IBNR deaths in the death data from WONDER. The reason for this is that the death data from WONDER are provisional: It can take several weeks for death records to be submitted to the NCHS, processed, coded, and then tabulated. Consequently, provisional data may be incomplete, especially for more recent time periods. Death counts for the latest weeks are revised regularly, and may increase or decrease, as data from new and updated death certificates are received. Importantly, for recent periods, death counts in WONDER data are incomplete and not the counts that will ultimately be observed; the CDC does not gross up initial values for IBNR deaths to estimate where they might ultimately land, and such estimates are not readily available. Actuaries (and other like-minded professionals) can develop reasonable gross-up factors through relentless data collection and tracking how initial death counts progress over long time frames. Importantly, this data monitoring and later data interrogation allows the application of sensible confidence intervals to recent estimates. Estimating IBNR requires a deep understanding of how death data are reported.

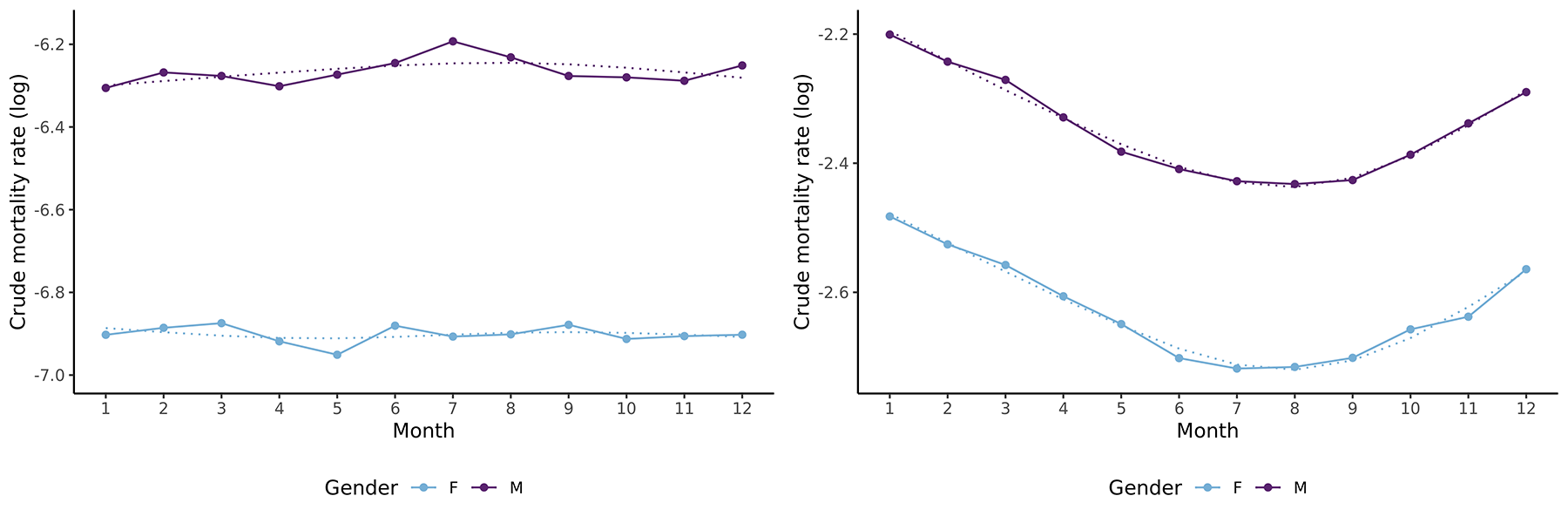

Considerations for expected mortality Quality and robust expected mortality rates are critical for useful analyses. They will determine excess deaths where: Excess deaths = Reported deaths + IBNR deaths - Expected deaths The expected deaths are what, before the pandemic’s onset, would have been anticipated for the current period, but still allowing for improvements (and seasonality if needed). For interested readers, this section sets out considerations for setting expected mortality rates. A typical approach to setting expected mortality rates is to set base mortality rates, then overlay estimated and projected improvements, and then overlay seasonality adjustments if the analyses are at a monthly or weekly level. This approach is useful for setting expected rates for both all-cause mortality and specific causes of death. It is necessary to consider how to group different causes in the data when setting expected rates by cause; less significant causes of death have mortality rates too volatile to work within this type of analysis. Mortality improvements must also be included to allow for a realistic view of any excess mortality that needs to be understood and explained. This more complete view informs the insights drawn from even short-term mortality changes and trajectories. Figure 2: Improvements in all-cause mortality for males and females at ages 35 and 85 for 2011-2023

Reasons to monitor US population mortality US population mortality datasets are sizable and updated regularly. They contain granular details such as date of death, age at death, and cause of death information, and are readily and freely available. As the US records around 3 million deaths per annum, the data offers an advanced and credible perspective on short-term mortality. During the height of the COVID-19 pandemic, monitoring excess mortality in real-time provided a comprehensive view of the pandemic’s impact beyond confirmed COVID-19 deaths and a better understanding of the crisis’ true toll. The excess death data included deaths indirectly caused by pandemic-related factors, such as disruptions to healthcare systems and economic hardships, and the longer-term effects of COVID-19 infection. In the current post-pandemic era, the observed short-term changes in excess mortality are offering insight into medium-term and possibly longer-term changes. These insights can be used as inputs to create frameworks, principles, and approaches to set future mortality assumptions. They can also be used to validate outputs from the given frameworks and estimates provided by actuarial associations. Such insights have always been critical for pricing protection business and annuities but have become more important than ever as the industry emerges from the COVID-19 pandemic.

Deviations between actual and expected death rates – i.e., excess mortality – were massive during COVID-19’s acute phase. Since exiting that phase, excess mortality has lessened, and as COVID-19 is now endemic, the population has a greater level of inherent immunity against severe outcomes. Nevertheless, it is also clear that 2023 mortality remained elevated relative to the pre-pandemic mortality expectation when allowing for improvements and seasonality. The challenge now is to understand how, given COVID-19’s impact, mortality will transition in the short-to-medium term to its long-term level, and what this long-term level might be. Life insurers, public health officials, and actuaries across various domains are proposing frameworks, principles, and even estimates of future mortality. Their goal: to bridge the gap between how future mortality assumptions were set historically and how they could (or should) be set now that the acute phase has subsided. (See “UK Mortality Projections: Practical implications of CMI proposals” as an example.1) A review of the many proposals and counterproposals reveals uncertainty around future mortality trends over the short-to-medium term as the new mortality regimes settle in. RGA has conducted a thorough analysis of emerging US population mortality data to identify how US mortality has changed through the pandemic, determine what it looks like in 2023 and 2024, and to understand where it may be headed in the coming years. This introductory article explores the following: Reasons to monitor emerging US mortality Data elements required to do so Considerations for these data elements Resulting insights that might be translatable to insured life mortality

Introduction Analyzing historic mortality to support assumption setting for future mortality is a challenging task – one made more difficult in the wake of the acute phase, starting in March 2020 and ending in March 2022 – of the COVID-19 pandemic. Data from the last few years is clearly not a reliable predictor of future mortality, and actuaries can no longer steer assumptions by just looking in the rearview mirror. Figure 1 reflects the challenges of using recent mortality data.

* Expected mortality rates come from an RGA-developed expected basis that uses US population mortality data from 2011-2019 inclusive. Improvement trends and seasonality are allowed for in the basis. The basis includes projected mortality rates for the 2020-2024 period which incorporate, and project improvement trends seen in the data. This basis is referred to as the “pre-pandemic expectation.” ** The standard population data used is the “2000 US Standard Population (Census P25-1130),” available here: https://seer.cancer.gov/stdpopulations/stdpop.singleages.html

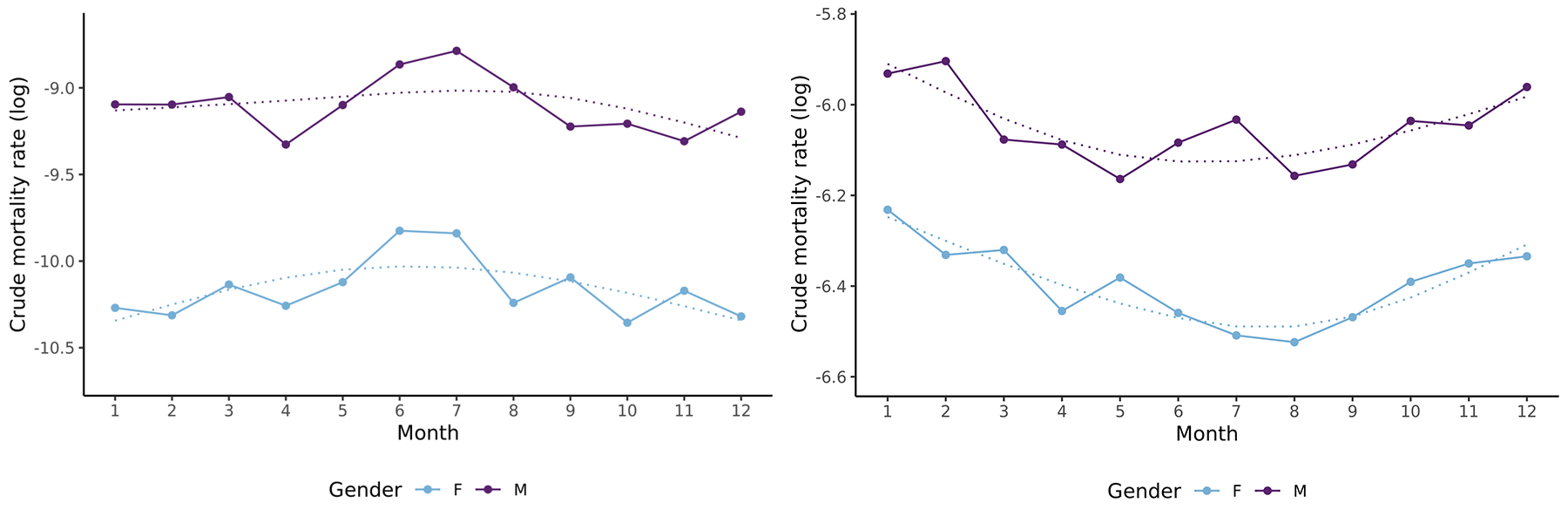

The graphs show the annual all-cause (log) crude mortality rates (dots joined by solid lines) by calendar month for lives aged 35 (left) and 85 (right) for both genders for the period 2011-2019 in the US. Smoothed curves are given by the dotted lines. Figure 4: Seasonality in “other accident” mortality for males and females at ages 35 and 85 for 2011-2019 The graphs show the annual (log) crude mortality rates (dots joined by solid lines) for the “other accident” cause of death by calendar month for lives aged 35 (left) and 85 (right) for both genders for the period 2011-2019 in the US. Smoothed curves are given by the dotted lines. The analyses that underlie the forthcoming full report use a pre-pandemic expected basis developed from the data described above. The expected bases are for all-cause and by-cause, and in all cases make allowances for improvement trends and seasonality. The improvements capture the trends observed in data and mortality rates are projected out for 2020 to 2024 with these trends. Extracting insured life insights Extracting insights for insured lives is a significant challenge when considering population-level mortality results. In many countries, for varied reasons, but notably underwriting, insured lives can have significantly different mortality levels from those of the general population. The differences in mortality among insured lives may also vary depending on the product and the provider. To translate population-level mortality insights into insured life insights requires a thorough understanding of a carrier’s book of business. Even then, appreciable uncertainty may remain and mandate the use of judgment. US population mortality data is a valuable data source. Challenges translating population-level insights to insured insights and to other countries are unavoidable given the US’s unique characteristics, such as its obesity epidemic, widespread opioid abuse, and lack of universal healthcare. That said, with the right data and approach, US population mortality can be a key source of granular and current mortality experience, and the emerging US results may provide leading insights into mortality trends in insured lives applicable to multiple markets.

Meet the authors

Post-pandemic US Population Mortality: How to track it and why it matters

By Brendon Lapham, Micah Canaday, Richard Russell, Jason McKinley, Michelle Haines, Dan Brandt, Ebrahim Steenkamp

Armstrong, C. (2023, April 24). Beyond the Pandemic: A driver-based view of mortality rates and their implications for actuaries. Beyond the Pandemic: A driver-based view of mortality rates and their implications for actuaries, RGA, Knowledge Centre. Retrieved April 24, 2024, from RGA Knowledge Centre: https://www.rgare.com/knowledge-center/article/beyond-the-pandemic-a-driver-based-view-of-mortality-rates-and-their-implications-for-actuaries https://www.cdc.gov/nchs/data_access/vitalstatsonline.htm https://wonder.cdc.gov/mcd.html https://www.census.gov/ https://www.soa.org/resources/research-reports/2023/rpec-mort-improvement-update/

References

RGA has conducted a thorough analysis of emerging US population mortality data to identify how US mortality has changed through the pandemic, determine what it looks like in 2023 and 2024, and to understand where it may be headed in the coming years.

Understanding how current mortality has changed compared to pre-pandemic expectations requires an expected mortality basis, i.e., some form of expected mortality, against which to measure. Expected mortality is critical to determining excess mortality and its likely trajectory.

To translate population-level mortality insights into insured life insights requires a thorough understanding of a carrier’s book of business. Even then, appreciable uncertainty may remain and mandate the use of judgment.

Figure 1: The four FIGO stages

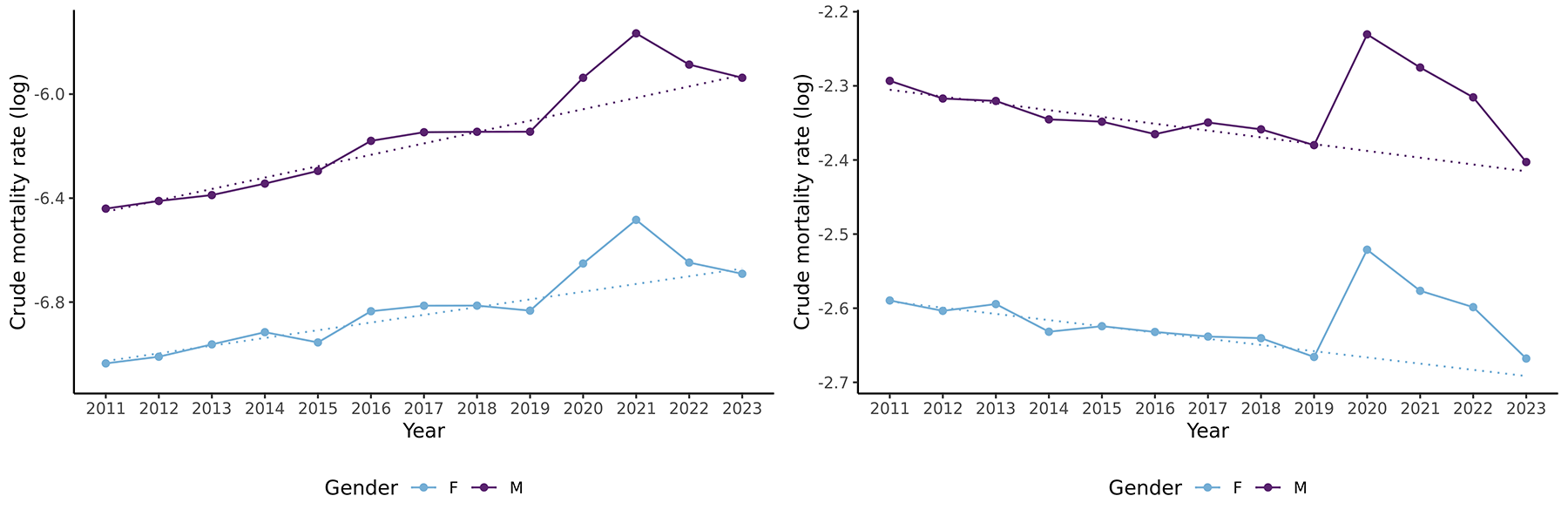

The graphs show the (log) crude mortality rates (dots joined with solid lines) for all-cause mortality for lives age 35 (left) and 85 (right) by gender and calendar year for the period 2011-2023 in the U.S. The dotted lines show the linear trends for the period 2011-2019 extended through to 2023. Estimates from the Society of Actuaries’ Mortality Improvement Model could be used for all-cause mortality.5 But wherever or however derived, it is important to ensure that improvements are aligned with base mortality rates and the data used. Mortality improvements will also vary by cause. Setting by-cause improvement assumptions will require judgement and pragmatism where the death data is sparse. Death data from CDC WONDER is available at annual, monthly, and weekly resolutions. The analyses carried out by RGA use a monthly resolution. This requires including seasonality adjustments in the expected basis, as significant seasonality is frequently observed at monthly levels in the US. Seasonality varies by age and is most pronounced for older lives for all-cause mortality, as illustrated in Figure 3 for all-cause mortality. That said, seasonality can be observed for younger lives when mortality is broken down by cause. For example, Figure 4 shows crude mortality rates for “other accidents” (non-transport accidents) and reveals elevated mortality for younger lives in the summer months. Figure 3: Seasonality in all-cause mortality for males and females at ages 35 and 85 for 2011-2019

Download

US Population All-Cause Mortality: Analysis by age and sex gives insight into reducing excess mortality

©2025 Reinsurance Group of America, Incorporated. All rights reserved. No part of this publication may be reproduced in any form without the prior permission of the publisher. For requests to reproduce in part or entirely, please contact: publications@rgare.com. RGA has made all reasonable efforts to ensure that the information provided in this publication is accurate at the time of inclusion and accepts no liability for any inaccuracies or omissions. None of the information or opinions contained in this publication should be construed as constituting medical advice.

By Jason McKinley, Richard Russell, Brendon Lapham October 2024

Jason McKinley Actuary in Global Research and Development.

Dan Brandt Vice President & Actuary, Experience Studies & Analytics, U.S. Individual Life

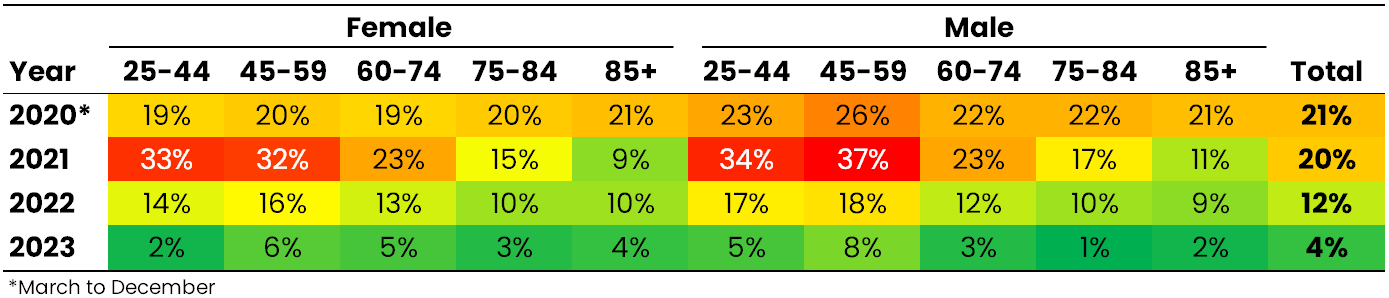

Key takeaways US population mortality is a key source of granular and current mortality experience. Emerging US results may provide leading insights into mortality trends for insured lives applicable to multiple markets and multiple functions within an insurer. These population trends might also signal the time when insurers can safely and reasonably redevelop new mortality bases from insured data. US excess mortality estimates for 2020 (March-December) and 2021 were 21% and 20%, respectively. This excess dropped to 12% in 2022 and 4% in 2023. We expect US population excess mortality to settle in the region of 1%-3% for 2024 overall; however, there is material uncertainty to this estimate – for one, 2024 has months remaining as of this writing. An overall excess of 1%-3% would be appreciably lower than the excess of 4% observed in 2023. Importantly, we demonstrate that age and sometimes sex differences significantly impact US population excess mortality estimates. Introduction Our introductory article addressed the importance of monitoring population trends as a leading indicator of insured mortality in uncertain times.1 We stressed the importance of using the right data and methodology to develop sound conclusions. Here we look at mortality experience in recent years to compare actual mortality with pre-pandemic expectations. We include age and sex breakdowns to reveal material differences in emerging excess mortality by these factors, which is especially important in translating population-level insights into insured-life insights. We distinguish between COVID and non-COVID deaths in this analysis; future reports will explicitly tackle specific non-COVID causes. Expected mortality rates are derived from an RGA-developed expected basis that uses US population mortality data from 2011-2019 inclusive. Improvement trends and seasonality are allowed for in the basis. The basis includes projected mortality rates for the 2020-2024 period, which incorporate improvement trends seen in the 2011-2019 data. This basis is referred to as the “pre-pandemic expectation.” The results presented here use publicly available data from the US Centers for Disease Control and Prevention (CDC) and the US Census Bureau (USCB). The CDC and USCB regularly update this data, so results presented in this analysis may change as new data becomes available. CDC 2023 and 2024 death data are provisional, and 2024 has months remaining as of this writing. We developed proprietary incurred-but-not-reported (IBNR) values based on several years' worth of weekly CDC data submissions and have applied these in the “2024 Outlook” statements below. Data changes in the exposures, additions to deaths (as the provisional results are made final), and variability in how IBNR develops add material uncertainty to the estimates. Acute phase all-cause mortality Mortality throughout the acute phase (defined here as occurring from March 2020 through March 2022) of the pandemic was dramatically elevated. The US population saw age-adjusted death rates (AADRs) 20% higher than expected, representing more than 1.1 million excess deaths; see Figure 1. By calendar year, acute-phase excess mortality was 21% for 2020 (March-December), 20% for 2021 (January-December), and 20% for 2022 (January-March); see Table 1. For 2020, excess was consistent across age bands, but in 2021 and 2022, younger lives experienced a larger burden of the excess. This additional burden was most prominent in 2021, when the Delta variant became dominant and had a much greater relative impact on younger-life mortality. Deaths attributable to COVID-19, defined as having COVID-19 appear anywhere on the death certificate,2 were the main contributor (~84%) to excess deaths during the acute phase. Figure 1: Monthly actual and expected age adjusted death rates (AADRs) for all ages (0-100) by calendar month for the pre-pandemic period February 2018-February 2020, the acute phase (March 2020-March 2022), and the post-acute phase (April 2022-April 2024) of the pandemic.

The relationship between population and fully underwritten insured mortality prior to and during the peak of the pandemic was clearly delineated in the seminal life insurance experience reports developed by RGA, the SOA, LIMRA, and TAI. COVID-19 is identified as the cause of death if it is the underlying cause of death or if it was among multiple causes of death. This definition is used throughout this research.

Notes

Public health officials are reluctant to officially proclaim the pandemic over, which is understandable given the 25,000+ COVID-involved deaths in 2024 in the US (as of this writing). But the acute phase, when the country sometimes experienced that many excess deaths in one week, has passed. The post-acute phase remains in flux, and various drivers of mortality are impacting age groups differently and, importantly, in different ways than in the recent past. 2024 Outlook: A preliminary estimate for excess in 2024 (January through April only) is 1%, which is lower than the excess of 2% for the same period in 2023, suggesting that excess mortality has continued to decrease in 2024; see Figure 2 and Figure 3. We expect overall US population excess mortality to settle somewhere higher than 1% by the end of 2024 — perhaps in the range of 1%-3% for 2024 in total, mainly due to the recent phenomenon of a shift forward in winter seasonal deaths among older lives. As noted earlier, there is sizeable uncertainty in this estimate, given CDC 2024 death data are provisional, and 2024 has months remaining as of this writing. Figure 2: Monthly actual and expected AADRs for ages 25-100 for females and males. The period shown is January 2015 to April 2024.

The post-acute phase of the COVID-19 pandemic remains in flux, and various drivers of mortality are impacting age groups differently and, importantly, in different ways than in the recent past.

Emerging US results may provide leading insights into mortality trends for insured lives applicable to multiple markets and multiple functions within an insurer.

Table 1: Age-adjusted excess mortality (actual AADR/expected AADR - 1) by sex, age band, and calendar year.

Figure 3: Total excess deaths (reported deaths + IBNR deaths – expected deaths) and reported COVID-involved deaths by month for ages 25-100 for females and males. The period shown is March 2020 to April 2024.

To understand where population excess mortality may be headed in the medium term, a comprehensive evaluation of each major cause of death is essential. We will examine some of the trends in specific causes in subsequent reports.

Ages 25 to 44 The US opioid epidemic predates the COVID-19 pandemic and continues today. Drug overdose deaths are most prevalent among the younger population. The historic rise in drug overdose deaths has translated to a negative improvement trend in population all-cause mortality at ages under 45 in the years leading up to the pandemic (2011-2019), which only worsened during the pandemic’s acute phase; see Figure 4. The negative trend did not discriminate by sex: The all-cause male annual dis-improvement rate was approximately 3.2% from 2011 to 2019 (the CDC officially declared the overdose crisis to be an epidemic in 2011), while female dis-improvement was approximately 2.1% per annum in that time frame. While the COVID pandemic provided additional headwinds in 2020 and beyond, COVID itself contributed much less to this group’s excess than the sum of all other causes; see Figure 5. Mortality in this age range peaked during the Delta wave of 2021, but for the first time in years in the US, this group appears headed toward three straight years of positive improvement. This welcome development may be largely attributable to an easing of mortality from drug overdoses. Indeed, the CDC recently reported that 2023 saw the first annual decrease in drug overdose deaths, across all ages, since 2018. Note: RGA’s US population mortality analysis will address this topic in greater detail as we explore specific causes of death in subsequent reports. Figure 4: Actual and expected AADRs for ages 25-44 for females and males. The period shown is January 2015 to April 2024.

Figure 5: Total excess deaths and reported COVID-involved deaths by month for ages 25-44 for females and males. The period shown is March 2020 to April 2024.

2024 Outlook: This age group has a large proportion of non-medical deaths. Non-medical deaths take many months longer to have a cause of death assigned. Our IBNR adjustments work best when cause of death information is available so the magnitude of excess for 2024 overall – in this age group – is still highly uncertain. That said, indications are that the 2024 age-standardized mortality will continue its drop since the 2021 peak. That is a remarkable turnaround, considering the previous trend and the worse-than-trend peak during the pandemic’s acute phase. Ages 45 to 59 For the decade preceding the pandemic, people aged 45 to 59 in the US experienced consistent cancer mortality improvements, which were countered by negative cardiovascular experience and increasing overdose deaths, resulting in largely stagnant improvements overall for most of the decade; see Figure 6. The trend of minimal year-to-year variance in the age-standardized all-cause mortality held steady from 2011 to 2019. The pandemic disrupted that trend beginning in 2020, but causes of death in addition to COVID contributed to the excess; see Figure 7. During the acute phase, this age group suffered particularly from a combination of metabolic disease deaths and increased cardiovascular deaths. In the post-acute phase, cardiovascular deaths have continued at a slower pace, but the suite of metabolic diseases has remained problematic, along with elevated cancer deaths. As of this writing, cancer and metabolic diseases are contributing more to the excess in this age group than COVID is. One tailwind for mortality in this and older age groups is the seeming displacement of pulmonary deaths, largely chronic obstructive pulmonary disease, that has been prevalent since the start of the pandemic. Figure 6: Actual and expected AADRs for ages 45-59 for females and males. The period shown is January 2015 to April 2024.

Figure 7: Total excess deaths and reported COVID-involved deaths by month for ages 45-59 for females and males. The period shown is March 2020 to April 2024.

2024 Outlook: Although still within the CDC provisional death data reporting period, the 2024 outlook is for excess to persist in this age group and possibly end the year between 3% and 5%. The predictability of this group pre-pandemic meant that projecting any excess over 1% would have been unusual, so projecting upward of 3% is unprecedented. Seasonality does not typically affect this age group as much as it affects older ages, so we do not expect an unusual end-of-year scenario moving that estimate much higher. Ages 60 to 74 Entering the pandemic, female mortality improvement was mildly positive (about 0.5% per annum) and male improvement was quite flat for this age group; see Figure 8. While males and females experienced similar excess mortality impacts during the acute phase of the pandemic, males have been returning to pre-pandemic expectations more quickly than females. Much of this difference is due to male cardiovascular deaths moving closer to pre-pandemic expected levels in 2023, while female cardiovascular deaths remained elevated. Female cancer excess also outpaces male cancer excess. COVID accounts for the largest share of excess in this age group, a situation that becomes increasingly prevalent with older ages; see Figure 9. Negative non-COVID excess has remained similar to that of the acute phase but is not as significantly offset by the positive excesses (COVID, etc.). Figure 8: Actual and expected AADRs for ages 60-74 for females and males. The period shown is January 2015 to April 2024.

Figure 9: Total excess deaths and reported COVID-involved deaths by month for ages 60-74 for females and males. The period shown is March 2020 to April 2024.

2024 Outlook: Males in this age group could return to pre-pandemic expectations in 2024. The good non-COVID experience seems to be largely offsetting the COVID deaths for males. The female outlook is not quite as positive. Males have a chance to record a better mortality rate than any they experienced in 2011 through 2019. Females accomplishing the same would require some extremely good results in the final few months of the year. More likely, males will end up within approximately 1%-2% of pre-pandemic expectation, with females over 2% higher. Ages 75 to 84 Almost all mortality trends for ages 60 to 74 apply to ages 75 to 84 as well, with the exceptions of the pre-pandemic annual improvement rates (around 0.8% for males and females) and some manifestations of causes of death over the acute and later pandemic phases; see Figure 10. In this age group, COVID has driven almost all excess mortality since the pandemic began; see Figure 11. The post-acute phase has seen a continuance of good experience from non-COVID excess as COVID itself has subsided. But for females in particular, the evidence of an uptick of cancer deaths has added to the all-cause story. Figure 10: Actual and expected AADRs for ages 75-84 for females and males. The period shown is January 2015 to April 2024.

Figure 11: Total excess deaths and reported COVID-involved deaths by month for ages 75-84 for females and males. The period shown is March 2020 to April 2024.

2024 Outlook: As with the 65-to-74 age group, males have a realistic opportunity to return to pre-pandemic mortality rates in 2024. Given the likely negative impact of seasonality, the more prudent forecast would anticipate slightly elevated male mortality, between 1% and 2%. For females, the outlook is slightly worse, with cancer remaining elevated above the very good pre-pandemic expectations. Ages 85 and Older For ages 85 and older, the pre-pandemic period was one of great mortality improvement – around 1.4% per year; see Figure 12. The pandemic impacted mortality for this age group the most, as advanced age often brings comorbidities and a limited ability to fight off intense infections. Cardiovascular deaths increased for this group, as did many other medical causes of death to a lesser extent. The only consistent bright spot was a decline in pulmonary deaths, likely displaced by COVID. This age group experienced three instances where excess deaths in one or more consecutive months topped 25%. Each of those instances was followed by a two-to-four-month period when all-cause experience was far better than the COVID mortality alone would dictate; see Figure 13. This may indicate accelerated deaths due to COVID that had a relatively immediate impact on the non-COVID causes in the aftermath of a large wave of COVID deaths. Figure 12: Actual and expected AADRs for ages 85 and older for females and males. The period shown is January 2015 to April 2024.

Figure 13: Total excess deaths and reported COVID-involved deaths by month for ages 85 and older for females and males. The period shown is March 2020 to April 2024.

2024 Outlook: COVID deaths hit this age group the hardest. That was true during the pandemic and remains true now, although the mortality impact has greatly diminished. As in the acute phase, COVID still appears to accelerate and displace deaths in this group, contributing to the non-COVID excess being generally quite good. Even cardiovascular deaths are approaching pre-pandemic expectations. But with flu season now underway, combined with the recent phenomenon of the seasonal increase in mortality for this age group starting earlier than expected (see Figure 12), we expect death rates in this group to remain a good deal higher than pre-pandemic expectations in 2024 – possibly around 2%-4% higher when the official statistics are available. What’s next RGA will continue to monitor US population mortality using the best data available and in near-real time, incorporating updates weekly and liaising with experts from the CDC, the USCB, and demographers as necessary. The results of this analysis are subject to change as new data becomes available. We have taken steps to reduce the likely impact of these changes, e.g., by including IBNR. In addition, this analysis combines multiple series of population estimates from the USCB, which requires incorporating adjustments to ensure smooth transitions across the different series. An upcoming change worth noting is the USCB’s release of the 2010 to 2020 Intercensal Estimates, with total figures slated for fall 2024 and age and sex breakdowns in late 2025. To understand where population excess mortality may be headed in the medium term, a comprehensive evaluation of each major cause of death is essential. We will examine some of the trends in specific causes in subsequent reports. To learn about the latest all-cause and by-cause report updates as they are published, sign up for RGA’s US mortality analysis email list.

Emerging all-cause mortality

Brendon Lapham Director, Data & Analytics Actuary, UK Pricing

Richard Russell Vice President, HBiometric Research, Global Research and Development

In brief In the wake of the COVID-19 pandemic, RGA has conducted a thorough analysis of emerging US population data to explore how all-cause mortality and excess mortality have changed through the pandemic, determine what they look like in the short term, and understand where they may be headed. While we have observed persistent excess mortality in the US population following the acute phase of the COVID-19 pandemic, recent mortality trends – including 2024 excess death estimates – suggest that the overall excess has decreased substantially from the peak of the acute phase. Indeed, there is a possibility that the age-standardized mortality – for some age groups and sometimes depending on sex – will be lower in 2024 overall than that observed in 2019 and in-line with pre-pandemic expectations for the period.

Perspectives from the RGA experts

U.S. mortality data perspectives

Underwriting: How US population death data helps us to understand the drivers of elevated mortality during the COVID-19 pandemic Catie Muccigrosso, VP & Chief Underwriter in USIL

Research & Development: How US population mortality data helped us monitor the immediate and ongoing impacts of the COVID-19 pandemic Richard Russell, VP in Global Research and Development.

“As we emerge from the acute phase of the pandemic, our analyses of US population death data have helped us unpick the drivers of ongoing excess mortality. For instance, many individuals with SARS-CoV-2 infection have symptoms that persist far beyond the immediate phase of the disease, sometimes lasting for years after the initial acute illness. Research has shown that among individuals hospitalized for COVID-19, risk of death declined but remained significantly elevated in the third year after infection. Further, the 3-year burden of cardiovascular disease in hospitalized survivors of acute COVID-19 is also substantial; this likely helps to explain why increases in cardiovascular mortality rates – observed at the height of the COVID-19 pandemic – endured well into 2023, despite the end of the public health emergency.”

CLOSE

“Population death data is an essential asset for our Global R&D team. The highly detailed death data available on CDC WONDER is especially valuable given its volume and granularity. During the COVID-19 pandemic, the CDC WONDER data offered us a near real-time opportunity to monitor both the direct and indirect death toll of the pandemic; like many researchers, we observed that the full impact of the pandemic was much greater than what was suggested by deaths due to COVID-19 alone. Our research – using CDC WONDER data – has also helped us to estimate the proportion of excess mortality that was a direct result of a SARS-CoV-2 infection. To apportion excess deaths into those directly attributable to SARS-CoV-2 infection and those indirectly associated with the "ripple effects” of the pandemic, multiple drivers of cause-specific mortality – and changes in these during the pandemic period – need to be carefully examined. One example of a significant change in cause-specific mortality, in the pandemic period, is the decrease in influenza deaths seen in the first three months of 2021. Another example is the count of deaths due to cardiovascular disease (CVD) – this grew significantly in 2020, from 874,613 CVD-related deaths recorded in 2019 to 928,741 in 2020.”

VP & Managing Actuary, Assumptions Lead in USIL

A wide range of RGA experts – in underwriting, pricing, risk management, insurance medicine, research and development, and more – have derived insights from this data analysis that they have applied to insured (individual and group life) and annuitant populations. Brief summaries of these insights and their ongoing value to RGA’s work can be found below.

Individual Life Actuarial “While US individual life mortality is typically thought of as being much lower than general population mortality, population mortality can still help inform assumption setting for insureds in certain areas.” Susan Willeat VP and Managing Actuary, Assumptions Lead in US Individual Life

Insurance Medicine “US population cause-of-death data helps us to monitor how past and present medical advances have driven down mortality rates, and project how cause-specific mortality rates will evolve in future years.” Dr. Daniel Zimmerman SVP and Chief Science Advisor

Mortality TRENDS “US CDC population death data can serve as a high-quality leading indicator of where insured mortality improvement may be headed.” Jason McKinley Actuary in Global Research and Development

Insurance Risk “Insured population mortality and morbidity assumptions need to be set in the context of the wider general population. The trends and changes observed within the wider population provide insights into some of the dynamics that may filter through to the insured population.” Elena Tonkovski VP and Senior Actuary, Insurance Risk

UNDERWRITING “As we emerge from the acute phase of the pandemic, our analyses of US population death data have helped us unpick the drivers of ongoing excess mortality.” Catie Muccigrosso VP and Chief Underwriter in US Individual Life

GLOBAL R&D ”During the COVID-19 pandemic, the CDC data offered us a near real-time opportunity to monitor both the direct and indirect death toll of the pandemic; like many researchers, we observed that the full impact of the pandemic was much greater than what was suggested by deaths due to COVID-19 alone.” Richard Russell VP in Global Research and Development

SVP and Chief Science Advisor.

Given reporting lags associated with group life data, US population mortality data provides early insights into emerging trends in the group life market. Further, cause-of-death data at more granular breakdowns by age and gender are more credible in the larger US population dataset. That said, we know group life mortality is lower than the general population, with the ‘SOA 2016 Group Term Life Mortality Study’ showing insured mortality at 30%-40% of population mortality in the key working ages. The actively-at-work requirement for employees covered by group life leads to a healthier subset and is the main driver for this differential. During the COVID-19 pandemic, insured mortality remained lower than population mortality, and excess mortality was directionally in line with the US population. By studying the relationship between recent insured and population excess mortality, actuaries can estimate population-to-insured factors to apply to projected population excess mortality. This in turn helps set assumptions for future expected excess group life mortality.

While US individual life mortality is typically thought of as being much lower than general population mortality, population mortality can still help inform assumption-setting for insureds in certain areas. One area is final expense, which generally serves a lower socioeconomic group very different from typical fully underwritten business. No current industry mortality table is even close to appropriate for final expense business. We have found that US population tables provide the best baseline table for developing our internal mortality assumptions for final expense. Final Expense mortality increases relative to population as age decreases. The US population baseline also provides useful perspective on the mortality for this unique market segment. US population mortality is also helpful in setting mortality assumptions for very high attained ages. US individual life mortality experience is clearly not as credible at very high attained ages as population experience. The question often arises: Will insured and population mortality eventually converge at some attained age? In other words, will the socioeconomic impacts that drive the difference between insured and population mortality disappear? One can use population mortality data split by a proxy for socioeconomic class to provide an indication of any convergence that could potentially inform assumption-setting at very high attained ages. By comparing the high attained age assumptions for each of our various market segments to a US population basis, we can easily review them for consistency.

GLOBAL R&D ”During the COVID-19 pandemic, the CDC data offered us a near real-time opportunity to monitor both the direct and indirect death toll of the pandemic; like many researchers, we observed that the full impact of the pandemic was much greater than what was suggested by deaths due to COVID-19 alone.” Richard Russell Vice President Biometric Research, Global Research and Development

US Population All-Cause Mortality: Excess mortality declines to 0.4% in 2024

By Richard Russell, Jason McKinley, Brendon Lapham August 2025

Key takeaways US population mortality is a key source of granular and current mortality experience. Emerging US results may provide leading insights into mortality trends for insured lives applicable to multiple markets and multiple functions within an insurer. These population trends might also signal the time when insurers can confidently and reasonably redevelop new mortality bases from insured data. Using an updated US population expected basis, we approximate that US excess mortality in 2024 was 0.4%, a significant reduction from the 3.2% estimated in 2023. Age and sex differences significantly impact US population excess mortality estimates. The 2023-2024 and 2024-2025 flu seasons had diminished impacts on 2024 mortality, with peaks occurring in late 2023 and early 2025, respectively; this helped drive down overall excess mortality in 2024. Introduction Our previous report presented US mortality experience in years 2020-2023, comparing actual mortality with pre-pandemic expectations. We also included “2024 outlook” statements suggesting where we expected overall US population excess mortality to settle by the end of that year. Here we review full-year 2024 excess mortality, including age and sex breakdowns, while separating COVID-19 and non-COVID-19 deaths. Expected mortality rates are derived from an RGA-developed expected basis that uses US population mortality data from 2011-2019 inclusive. The baseline for comparison is a key assumption when calculating excess deaths. Expected mortality rates can be produced in numerous ways and will determine the excess results derived – read more about this in our introductory report. In this current report, we have revised the expected basis, providing an updated assessment of the excess deaths that have occurred. The prior basis included projected mortality rates for the 2020-2024 period and incorporated seasonality and improvement trends observed in the 2011-2019 data. March 2025 marked five years since the pandemic officially began. It is questionable whether estimates of excess mortality based on extrapolations of pre-pandemic mortality trends remain sensible over such an extended period. Consequently, we now include age- and sex-specific long-term rates (LTRs) of mortality improvement, reached after age- and sex-specific convergence periods, in the expected basis. LTRs were derived using average annual improvements observed in the US from 1933 to 2023; mortality rates were taken from the Human Mortality Database. While the expected basis again includes seasonality and begins with the trends supported by the 2011-2019 data, expected mortality rates now converge toward LTRs. One additional, important update to the basis is our incorporation of the US Census Bureau’s (USCB’s) 2010-2020 intercensal population estimates, which were released in late 2024. The results presented here use publicly available data from the US Centers for Disease Control and Prevention (CDC) and the USCB. The CDC and the USCB regularly update this data, and results presented in this analysis may change as new data becomes available.

Figures 2 and 3 clearly illustrate that – for ages 25-100 – all-cause AADRs and COVID-19 deaths continued to decline in 2024, resulting in a substantial decrease in excess mortality. In our last report, we suggested that excess mortality might settle in the range of 1%-3% for 2024 in total, mainly due to the recent shift forward in winter seasonal deaths among older lives. However, the 2023-2024 and 2024-2025 flu seasons had diminished impacts on 2024 mortality as they peaked in late 2023 and early 2025, respectively; this helped drive down excess mortality in 2024.

These population trends might also signal the time when insurers can confidently and reasonably redevelop new mortality bases from insured data.

Ages 25 to 44 Mortality trends among early adults in the US were recently reported by Wrigley-Field et al.; as in our report, the researchers showed that mortality rates in early adulthood (ages 25-44 years) have risen substantially in two stages: 2011-2019 and 2020-2023; see Figure 4. From 2011 to 2019, we estimate that all-cause male annual dis-improvement was approximately 3.2%, while female dis-improvement was approximately 2.1% per annum. A significant rise in drug overdose deaths in this period helped fuel a large increase in all-cause mortality for this age group. The rise only worsened during the pandemic’s acute phase. As predicted in our previous report, this age group has now achieved three straight years of improvement. A clear and obvious decline in mortality rates started after the acute phase of the pandemic; however, excess mortality remained higher than expected based on pre-pandemic levels in 2023. Using an updated expected basis, we estimate that 2023 excess mortality was 7.1% in females and 11.0% in males. These estimates are higher than we previously reported due to the convergence to LTRs in our existing expected basis. The research by Wrigley-Field et al. indicated that the largest fraction of 2023 excess mortality was due to drug poisoning, but many other external and natural causes of death surpassed what historic trends would have projected. COVID-19 itself contributed much less to this group’s excess than the sum of all other causes; see Figure 5.

2024 excess: Remarkably, 2024 AADRs in this age group nearly returned to 2019 levels for men and women. This is an astonishing recovery, considering the 2020-2023 trend, with significant year-on-year dis-improvements. Indeed, using the updated expected basis, we estimate that 2024 excess mortality ran negative: -1.9% in females and -1.7% in males. There remains a long way to go for this group to achieve what could be considered favorable mortality, but the 2024 result is a basis for cautious optimism. Ages 45 to 59 From 2011 to 2019, AADRs in this age group were quite flat. The pandemic disrupted this trend; see Figure 6. During the acute phase of the pandemic, 45-to-59-year-olds suffered increased cardiovascular and metabolic disease deaths; research studies indicate that the pandemic exacerbated existing health issues, leading to more severe cases and higher mortality rates in individuals with these pre-existing conditions. Emerging from the public health emergency, excess cardiovascular deaths have continued at a slower pace while metabolic diseases have remained elevated, along with cancer deaths. In 2023, excess mortality was 5.8% for females and 9.6% for males; non-COVID-19 causes of death make up most of the excess, especially in males; see Figure 7.

2024 excess: Excess mortality in 2024 remained sizeable in this age group: 2.5% in females and 4.0% in males. COVID-19 was only a small contributor to the observed excess, with cancer and metabolic diseases being the most important drivers Ages 60 to 74 The 60-to-74-year-old cohort is a significant segment of the overall US population, often referred to as the “young-old” within the broader category of older adults. Recently published USCB data shows that, as the US population continued to age, the share of the population aged 65 and older increased from 12.4% in 2004 to 18.0% in 2024. Mortality improvements, 2011-2019, have been minimal for this age group. AADRs have followed a strikingly comparable pattern for females and males in the period 2015-2024; see Figure 8. Furthermore, the pattern of excess mortality experienced between females and males is most similar in this age group compared to other age groups; see Figure 9. Using our updated expected basis – with the inclusion of LTRs – reveals that the excess mortality estimate for males increased in 2023; our latest estimates of 2023 excess mortality are 5.2% for females and 4.5% for males.

2024 excess: Excess mortality in 2024 continues to be significant in this age group: 3.9% in females and 2.6% in males. On the other hand, 2024 AADRs in this age group are very close to pre-pandemic levels for both men and women. Ages 75 to 84 The leading causes of death for this age group are very similar to the 60-74 age group, although pre-pandemic annual improvement rates have been higher in 75–84-year-olds. In the period 2011-2019, per annum improvements in AADRs were 0.8% for males and females; see Figure 10. In this age group, COVID-19 has driven almost all excess mortality since the pandemic began; see Figure 11. Adjustments to the expected basis have had minimal impact on our previously reported excess mortality estimates. In 2023, excess mortality was 2.6% for females and 0.7% for males. The post-acute phase has seen a continuance of good experience from non-COVID-19 causes of death while COVID-19 mortality has slowly subsided; see Figure 11.

2024 excess: Excess mortality in 2024 was quite different by sex: 1.5% in females and -0.8% in males. Minimal mortality burden from the past two flu seasons helped drive down excess mortality. Importantly, 2024 AADRs – in both men and women – are at levels lower than observed pre-pandemic. COVID-19 continues to be an important factor. The higher excess in females relative to males appears to be a consequence of a material rise in cancer deaths; modeling studies support the hypothesis that declines in breast cancer screening and diagnosis during the pandemic could have material impact on cancer mortality in this timeframe. Ages 85 and Older Incorporating the USCB’s latest population estimates in our expected basis has had a material impact on the excess results for this age group. This is due to a significant change to our population exposure estimates in persons aged 85 and older. Prior to the pandemic, this age group experienced substantial mortality improvement – around 1.4% per year in the period 2011-2019; see Figure 12. This age group was the most vulnerable to COVID-19; according to the CDC, the death rate for COVID-19 among adults aged 85 and over (1,645.0 per 100,000 population) was 2.8 times higher than the rate for ages 75–84 (589.8), and seven times higher than that for ages 65–74 (234.3) in 2020. While COVID-19 mortality rates in this age group decreased significantly over the course of the pandemic, they remained higher in 2023 than those for all other age groups. As in the acute phase, COVID-19 still appears to somewhat accelerate and displace deaths in this group, as indicated by the peaks in COVID-19 deaths followed by troughs in total excess deaths; see Figure 13. Using our updated expected basis, we now report significantly different estimates of 2023 excess mortality: 1.4% in females and -2.3% in males. These estimates are much lower than our previous figures, given that we now reflect updates to the USCB’s population estimates as well as convergence to LTRs.

2024 excess: Older adults, especially those aged 85+, are at a significantly higher risk of severe complications and death from influenza. Seasonal influenza’s impact on all-cause mortality varies from year to year, with more severe seasons leading to higher mortality rates. The 2024-2025 influenza season in the US has been classified as “high severity” – the first high-severity designation since the 2017-2018 season. Our previous report suggested that, due to concerns around the mortality burden of the 2024-2025 flu season, excess mortality and AADRs in this age group might remain higher than pre-pandemic expectations in 2024. The 2023-2024 and 2024-2025 flu seasons had diminished impacts on 2024 mortality in this age group, as they peaked in late 2023 and early 2025, respectively. This has certainly eased overall excess mortality in 2024. AADRs have returned to pre-pandemic levels for both men and women. Indeed, male AADRs are the lowest we have ever observed. Consequently, our excess mortality estimates for 2024 are: -0.2% in females and -4.9% in males. What’s next RGA will continue to monitor US population mortality using the best data available and in near-real time, incorporating updates weekly and liaising with experts from the CDC, the USCB, and demographers as necessary. The results of this analysis are subject to change as new data becomes available. To understand where population excess mortality may be headed in the medium term, a comprehensive evaluation of each major cause of death is essential. We will examine some of the trends for specific causes in subsequent reports. To learn about the latest all-cause and by-cause report updates as they are published, sign up for RGA’s US mortality analysis email list.

All-cause mortality trends by age and sex

In brief Excess mortality during the COVID-19 pandemic has been considerable. Understanding excess death rates in the aftermath of the global public health emergency remains essential to assess its lingering burden. In this report, RGA has updated its analysis of US population data to understand how all-cause excess mortality settled in 2024, the fifth year of COVID-19. While we have observed persistent excess mortality in the US population following the acute phase of the COVID-19 pandemic, recent mortality trends suggest that all-cause mortality rates have continued to decrease substantially, with 2024 total excess mortality settling at just 0.4%. Minimal mortality burden from the past two flu seasons – impacting the 2024 calendar year – helped drive down excess mortality. Age and sex differences significantly impact US population excess mortality estimates, which suggests the underlying drivers of persistent excess mortality vary based on these factors. To understand where population excess mortality may be headed in the medium term, a comprehensive evaluation of each major cause of death is essential. RGA will examine some of the trends in specific causes in subsequent reports.

A return to widespread mortality improvements is a welcome sign after so much loss of life during the acute phase of the COVID-19 pandemic. Yet even this good news brings its own challenges. With life expectancy again on the rise, the risk of people outliving their savings increases accordingly, creating financial pressure for both individuals and governments. Insurance protection is essential to help fill the gap. In a recent Fortune interview, RGA President and Chief Executive Officer Tony Cheng outlines the industry’s vital role in ensuring long-term financial security and the need to educate the public on the benefits of insurance in retirement:

“On the longevity side what [longer lifespans] could unearth—which I believe one day will happen—is the consumer’s stronger awareness that unfortunately people may outlive their savings. And that’s scary.” This realization will also likely come “quite slowly” and “probably too late”, Cheng added: “If government budgets get more stretched—the amount you can get from the government one would think it’s going to be less over time, hence the need for more private funding.” “So that realization is an insurance gap, what I would call longevity insurance gap, that we educate on but people [would] rather take a lump sum usually than get paid a pension for the rest of their life. That’s a human trait.” He continued: “The government has to educate, the consumers actually have to listen and be educated. And then the business is obviously the big engine that gets it going.”

With decades of experience enabling insurers to provide life, health, and longevity protection, RGA is ready to help your business get up to speed to meet evolving consumer needs. Contact us today.

Filling the longevity insurance gap

In a recent Fortune interview, RGA President and Chief Executive Officer Tony Cheng outlines insurance’s vital role in ensuring financial security for longer lifespans.

All-cause mortality by period US population age-adjusted death rates (AADRs) by pandemic period are shown in Figure 1. By calendar year, acute-phase excess mortality was 21.0% for 2020 (March-December), 18.8% for 2021, 11.3% for 2022, 3.2% for 2023, and 0.4% for 2024; see Table 1. Note: Some excess estimates are different than those published in our previous report, given the changes to the expected basis as described above.